Tax Free Savings Account (TFSA)

What's in mine

Hi Money makers,

Welcome to TalkingCents, a weekly newsletter about finance, investment, and economics. If you’d like to learn more, you can join the community by clicking here.

In today’s article, I’m going to be showing you what’s inside my Tax Free Savings Account (TFSA) and why I have chosen the respective ETFs.

WHAT IS A TFSA?

In 2015, The National Treasury introduced a new long-term savings vehicle for South Africans known as the Tax Free Savings Account (TFSA). The aim of this new vehicle was/is to encourage and improve the savings rate of South African citizens.

A TFSA allows an individual to invest in various asset classes without having to pay income tax, dividends tax, or capital gains tax on the returns from these investments. There is one caveat to this, which I’ll explain further down in this article.

The annual limit for individual investors is currently R36,000 and the lifetime limit per investor is R500,000. Your annual contribution(s) MUST NOT exceed the individual limit of R36,000 in any given tax year, as any contribution(s) over and above this amount are taxed at a rate of 40%.

The tax year in South Africa runs from 1st March - 28th February.

Look at an example below:

Government initially maintained the threshold at R30 000, but they do increase these limits from time to time. I believe they will continue to do so in the subsequent years ahead when many get closer to that R500 000 contribution limit.

Let’s look at an example of someone who over contributes to their TFSA:

“Investor A”

Contributes R30 000 in the 2021 tax year. They did not max their allowance out of R36 000. They now forfeit the benefit because they cannot rollover the R6000 into the following 2022 tax year.

They have missed the opportunity to max it out for that tax year. They don’t now get R42 000 in the following tax year. The allowance will reset to R36 000 again in the following tax year (1st March).

“Investor B”

Over contributes to their TFSA account in 2021. Instead of paying R36 000, they paid R50 000 (R14 000 extra than what is allowed).

“Investor B” contributed R14,000 above the annual limit of R36,000 and will be subject to a tax rate of 40% on the over-contribution. They cannot reduce the following years contribution either because it will reset again to R36 000.

Investor A would miss out on maxing out their allowance for that tax year, and Investor B would have to pay R5600 in penalty fees for their over contribution of R14 000.

Can an individual have more than one TFSA?

Any person (including minor children) may have more than one Tax Free Savings Account, however, the annual limitation is still R36 000. If you decide to have two TFSAs, that doesn’t mean you now get R72 000, it means that each one could get up to R18 000. The annual limitation is an aggregation per year of assessment.

Key things to remember

The Tax free Savings Account name is a bit ambiguous because it can be deceptive. Savings accounts are usually considered short-term instruments for short term goals.

However,

this investment vehicle shouldn't be used as a short-term savings account but should rather be treated as a long term investment account that supplements ones main retirement investment account.

This is because any withdrawals from this account (TFSA) reduces your lifetime limit. Any funds withdrawn cannot be replaced and it then permanently reduces your TFSA limit going forward.

Make sure when you are putting money inside this account, you are ready to leave it there for no less than 15 years.

Why You should consider it

It’s not often that we get a gift from government, so this is something we should all be trying to utilize because as it says in the name, interest tax, dividend income and capital gains tax are all exempt. (Tax free)

This brings me to the caveat I mentioned earlier, the tax free doesn’t apply to foreign dividends. This means any ETFs holding foreign paying constituents in their fund will still be subject to tax in the judication that that constituent is based in.

Your Tax Free Savings Account is only applicable to South African holdings, you can’t not pay tax on foreign holdings because those companies are not part of South Africa, so our law cannot over rule another country’s tax law. However, you will still benefit from the capital appreciation of the ETF and will be exempt from capital gains tax inside the TFSA.

If you were wanting to truly maximize the benefits of a TFSA, you’d want to be invested into local paying dividend ETFs. There is a good and bad side to this strategy. Your account within your TFSA should consist of local and foreign concentrated ETF’s.

Let me explain:

MY TOP TFSA PICKS

It’s nearly that time of the year again where the financial tax year ends (28th February). If you haven’t maxed out your TFSA account yet then now would be a great time to try and do so before the new tax year begins on the 1st of March 2022.

After the 28th February 2022, a new tax year will begin and you will forfeit your allowance if it hasn’t been maxed out. Your tax allowance will reset to R36 000 again, as in the examples I showed above.

With that being said, lets take a look at what I have inside my TFSA:

CoreShares Global DivTrax (GLODIV)

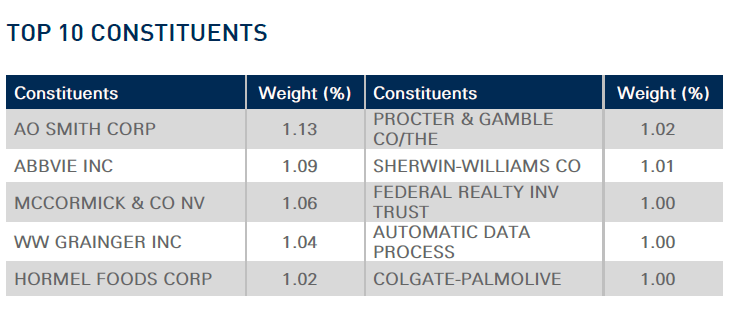

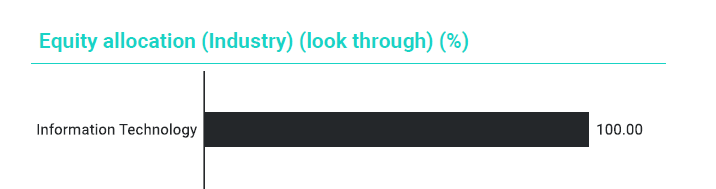

1nvest S&P500 Info Tech (ETF5IT)

CoreShares Preference Share Exchange Traded Fund (PREFTX)

Number 1:

What I like abut this ETF is that it has strong liquid constituents inside, making it easier to buy and sell (getting in and out) the ETF.

The companies have strong brand presence and usually benefit well in all economic cycles. The bonus is that many of these companies pay dividends too, although these are foreign companies, which means you’ll be taxed on dividends at the prevailing tax rate in those judications even though it’s in your TFSA.

It is a well-diversified ETF with global exposure. It’s focused 100% on outside of South Africa and offers a great hedge against the Rand. Meaning if the Rand were to continue to depreciate, you’d have a steady Rand hedge to complement your portfolio.

The fund was launched in February 2018 and listed at R9.60. It closed on Friday the 11th February 2022 at R16.17 (68% return).

Click here for the full Fund Factsheet

Number 2:

It would be wise to continue watching this ETF because as the sell off in the US markets continue it will bring down the price of this ETF. Offering you an ideal opportunity to add to your portfolio or to start building a position in high quality stocks.

We may be in luck where the dips in US stocks coincides with a new tax year for us.

I like this ETF because it offers me protection against a depreciating Rand while giving me exposure to companies that generate positive cash flow and earnings.

Please be aware that it focuses entirely on one sector only, the Information Technology sector. That means there is a concentration risk and drawdowns can be more significant in these types of ETF setups, especially if that sector becomes unloved.

You should be able to handle volatility well if you decide to pick a fund like this. It is an aggressive fund that should be held for no less than a period of 5 years. Returns in these funds usually do well in the long run and usually outperform other more risk averse investments.

Below you’ll be able to take a look at the overall performance.

The fund was launched in March 2018 and listed at R4.66. It closed on Friday the 11th of February 2022 at R15.18. (225% return)

For the full Fund Factsheet click here:

Number 3:

What I like about this fund is the income component. It is entirely focused on South African companies that pay dividends, making it ideal for benefitting from dividends tax.

When we talk about the TFSA and its benefits, we are referring to ETFs like these that offer the trifactor - free from income tax, dividend tax, and capital gains tax.

However, as you will see, the performance of this fund has been lacklustre. You may be benefitting from the dividend tax side of it, but the capital appreciation of the fund is slower that other global ETFs.

So although you gain from the dividends side, it is pulled down by the funds performance in the long term. Leaving you to question if the dividends are even worth it.

The fund was launched in December 2013 and listed at R10.87. It closed on Friday the 11th of February 2022 at R10.02 ( -7.8%).

For the full Fund Factsheet click here:

Trading within your TFSA

This may be a bit unorthodox, but I use my TFSA account to trade ETF’s sometimes. I buy some ETFS within my TFSA with the intention to sell them in a few months once they have rallied. Then I take the profits and I put them into my longer term ETF holdings.

ETF’s move similar to shares, but more slowly over the long term. The companies inside of them go through cycles, therefore this cycle tops and bottoms will play out in the respective ETFs too.

Take a look at PREFTRAX below.

We know that from 2013 till today it has performed terribly, delivering a negative 7% return.

Why would I want to hold it for the long term then? For the dividends?

That’s not enough for me. I want the dividends and the capital appreciation. This is why I try to buy low and sell high, as depicted in the picture below.

Blue circles are buy areas, and yellow circles are sell areas. After the next pullback I will buy again and then sell after another rally, while trying to benefit from dividends in between.

Why wouldn’t I try to do this? I have a free pass in my TFSA account to try.

Watch the full video below for a more detailed report.

Stay safe, everyone

See you next week :)

Hi Vinesh,

Sorry, I never put the weighting in the article, but I did share that information in the video on YouTube.

My weightings are as follows:

+- 60% - GLODIV

+- 30% - ETF5IT

10% - PRETAX

I have a stronger weighting to offshore exposure.

Hope this helps. 😊

Maybe I missed it but I didnt see any results of how the choice of shares have performed over the years. You have given your selection of etfs and their individual performance but not their weighting in your TFSA. What if 90% was allocated to the share the last one that has only done 8.6% since inception.