Hi Money makers,

Welcome to TalkingCents, a weekly newsletter about finance, investment, and economics. If you’d like to learn more and be part of the community, then you can join by clicking here.

In today’s article I’m going to be talking about the differences between unit trusts and ETFs.

What’s the difference?

Both Unit Trusts and ETFs are pooled investment products, or collective investment schemes. The key difference between ETFs and unit trusts is how investors buy and sell their units or shares within each investment product.

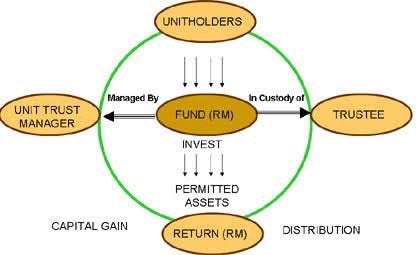

In unit trusts, money is collected by the fund manager from many investors to invest in securities like stocks, bonds, and other assets. This investment vehicle is set up under a trust structure.

The investor is effectively the beneficiary of the trust.

Fund managers run the unit trust and trustees are often assigned to ensure that the fund is run according to its goals and objectives. A unit trust's success depends on the expertise and experience of the company that manages it.

ETFs

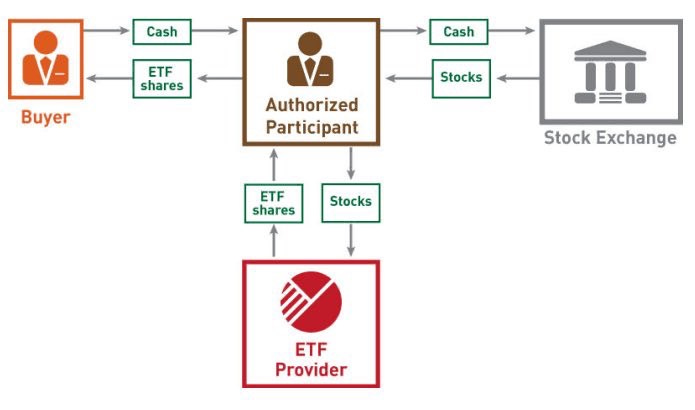

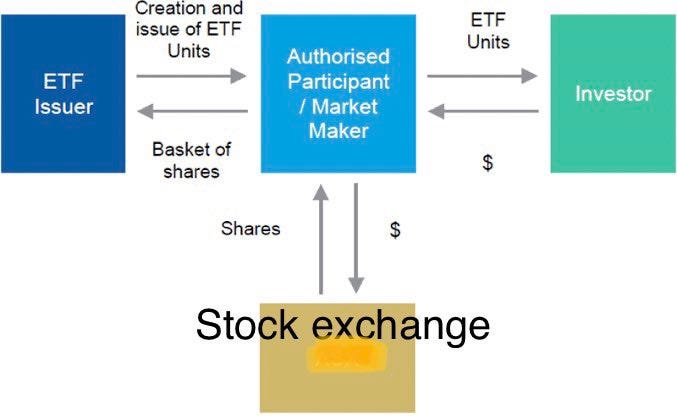

Exchange Traded Funds (ETFs) are traded like a stock throughout the day on the stock exchange. Shareholders of ETFs do not directly own shares of the underlying securities or assets, but rather, they own shares of the ETF itself.

An ETF issuer must have an agreement with a market maker before it can begin trading. The market maker provides liquidity by acting as both a buyer and seller of ETF units

ETFs will track a particular index, sector, commodity or other asset.

For example:

• S&P500 index ( SPY 0.00%↑ )

• Nasdaq ( QQQ 0.00%↑ )

Here’s a list of more examples:

Fees

There are three important fee structures to take note of when choosing to invest in an ETF or a Unit Trust:

1. Expense Ratio

2. Brokerage fee

3. Trading costs

1. Total Expense Ratio (TER)

An ETF and/or Unit Trust’s expense ratio is the cost to operate and manage the fund. These include:

• Management fees

• Administrative fees

• Operating costs

This is deducted from a fund’s net asset value (NAV)

2. Brokerage Fees

These are fees charged by banks, financial advisors, or brokers for executing the transaction of an ETF or unit trust.

3. Trading costs

These are other costs that aren’t covered in the TER.

Such as:

• Brokerage commissions

• Bid-ask spreads

ETFs

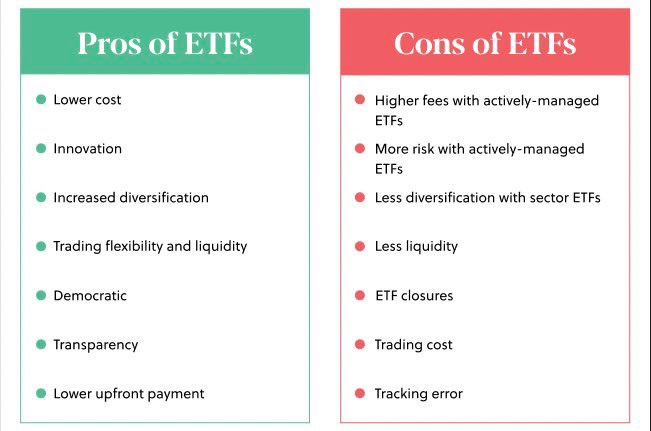

The benefits of investing in an ETF:

Offers diversification

Is liquid, meaning you can get your money out a lot easier and quicker.

Lower in costs

The negatives of investing in an ETF:

There can be tracking errors

It is an actively managed fund, which can increases the fees. You can also choose a passively managed fund.

There are trading costs from buying and selling.

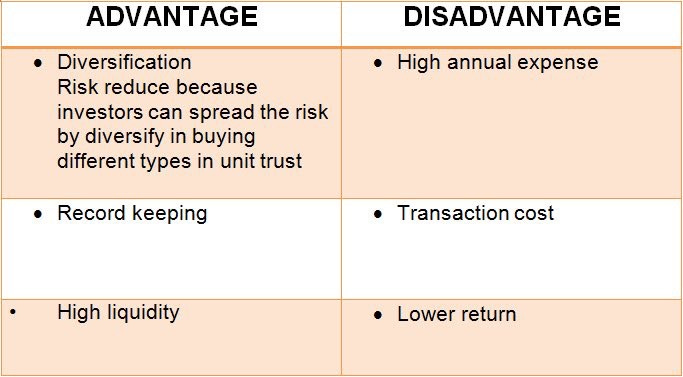

Unit Trusts

The benefits of investing in a Unit Trust:

It is an affordable option, because there is less buying and selling.

There is a professional management team overseeing the fund.

Transparent, regulation requires everything to be made available.

The negatives of investing in a Unit Trust:

Can also be costlier than compared to ETFs

End of day purchases, meaning buying and selling occurs at the end of day.

Illiquid at times, meaning you might wait a while to get your money out and back into your own account.

Key Takeaways

• ETFs offer more diversification, while unit trusts allow investors to pick securities

• ETFs are managed passively while Unit Trusts are managed actively (both can apply)

•Investing in ETFs is usually less expensive than Unit Trusts

•ETFs are usually more liquid than Unit Trusts

My personal opinion,

I’d rather opt for ETF’s with a very low TER that tracks an index or a particular sector, while constantly adding to it no matter what the market condition is like. Over the long term, in the right ETF, you’ll outperform many professional investors.

This is what I do in my Tax Free Savings Account (TFSA)

Remember this,

investing isn’t meant to be sexy.

Stay safe, everyone

See you next week :)